Viewpoints

Industry insights, market outlook reports and commercial real estate

news, and trends from the Coldwell

Banker Commercial brand.

News

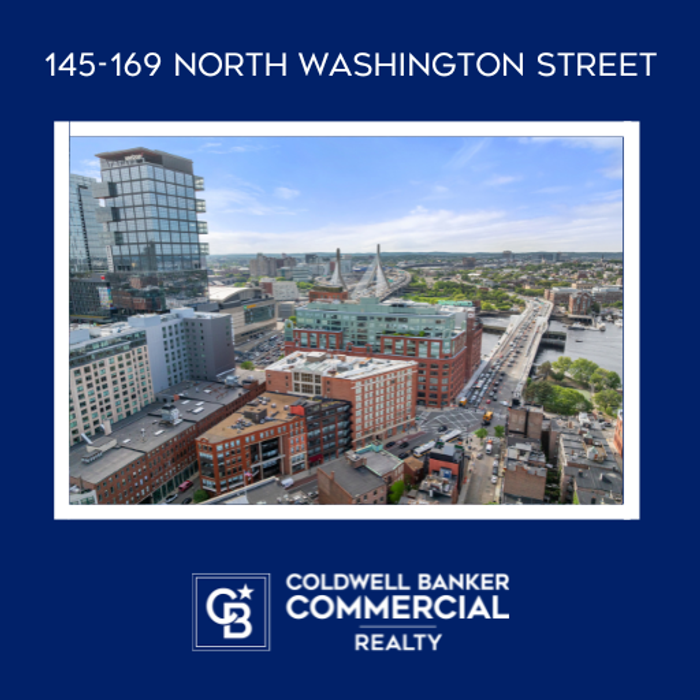

Premier Development Opportunity Hits the Market in Downtown Boston

Jul 2, 2025

Explore a rare development opportunity at 145-169 North Washington Street in downtown Boston—over 6,000 sq ft of prime land with existing buildings and parking, ideal for residential, hospitality, or mixed-use projects in a AAA location.

Latest Viewpoints

See all Articles >

News

No. 1 Coldwell Banker Commercial Broker Dan Mcgue Closes On Two Trophy San Francisco Apartment Buildings Totaling $19M

Jul 2, 2025

Top Coldwell Banker Commercial broker Dan McGue closes two prime San Francisco apartment buildings for $19M, adding to his $3.3B+ career sales volume. Discover the details of these high-profile multifamily transactions.

Read More >>

Industrial

Industrial Real Estate: Resilience in a Cooling Economy

Jul 2, 2025

Despite broader economic uncertainty, the industrial real estate sector remains resilient, supported by strong fundamentals and evolving demand drivers like e-commerce, AI infrastructure, and supply chain reconfiguration. Green Street’s latest Commercial Property Outlook reveals why industrial assets continue to offer compelling, risk-adjusted returns in a cooling market.

Read More >>

Podcasts

In Case You Missed It: June 2025 Recap

Jul 1, 2025

In this ICYMI, we highlight some new technology partnerships, learn how we celebrate our best of the best, discuss our partnership with Realtors Land Insititute and more.

Read More >>

Insights

Excel and AI Usher in New Era of Commercial Real Estate Business Intelligence

Jun 25, 2025

AI-powered Excel is revolutionizing commercial real estate by simplifying complex data analysis, automating financial modeling, and enhancing decision-making across leasing, investment, and property management. With tools like Excel 4 CRE and natural language processing, CRE professionals can unlock deeper insights, streamline workflows, and gain a competitive edge in today’s data-driven market.

Read More >>

News

Coldwell Banker Commercial Premier Welcomes Nick Till, Experienced Commercial Real Estate Executive

Jun 20, 2025

Coldwell Banker Commercial Premier proudly welcomes Nick Till, a seasoned commercial real estate executive and licensed general contractor, to its Las Vegas team. With over 20 years of expertise in land acquisitions, investment properties, and industrial development, Till brings strategic insight and proven results to Southern Nevada’s dynamic CRE market.

Read More >>

Insights

2025 Elite | Top 2 Event

Jun 17, 2025

Coldwell Banker Commercial honored its Top 2% professionals and Commercial Elite companies with an exclusive retreat in Park City, Utah, celebrating excellence with curated experiences and meaningful connection. Discover how CBC fosters belonging and recognition through this unforgettable annual event in a serene, boutique setting.

Read More >>Trend Reports

See all trend reports>-

trends

trendsThe Trend Report: C-Store Evolution - From Snacks to Supermarkets and Beyond

Apr 1, 2025Convenience stores (c-stores) have evolved significantly since their urban beginnings in the 1920s, adapting to meet the needs of an...

Read More >> -

trends

trends2025 Outlook Report: Expect Recovery to be Uneven Across Property Types and Locations

Feb 11, 2025Commercial real estate faced significant challenges in early 2024 due to delayed interest rate cuts, election uncertainty, inflation, and stricter...

Read More >> -

trends

trendsThe Trend Report: Fall 2024

Nov 13, 2024Coldwell Banker Commercia's Trend Report Fall 2024 highlights the evolving housing market dynamics, driven by low mortgage rates and millennial...

Read More >>

Latest CBC Podcasts

Listen and learn from the Coldwell Banker Commercial brand on this commercial real estate focused podcast.

-

Jul 1, 2025

Jul 1, 2025In Case You Missed It: June 2025 Recap

In this ICYMI, we highlight some new technology partnerships, learn how we celebrate our best of the best, discuss our partnership with Realtors Land Insititute and more.

-

Jun 17, 2025

Jun 17, 2025Martket Tales: Hartford, CT

In this episode of the CRE with CBC Worldwide Podcast, Ashley Wilson interviews Brandon Rush, a commercial real estate professional from Hartford, Connecticut. Brandon shares his journey from a technology background to becoming a successful...

-

Jun 3, 2025

Jun 3, 2025In Case You Missed It: May 2025 Recap

In the May 2025 edition of the Coldwell Banker Commercial podcast, the team celebrates the achievements of their professionals, highlights educational opportunities, and introduces new tools like RCA for enhanced data access. We reflect on...

Work with a CBC

professional for expert

guidance on all your

commercial needs.