2022 MID-YEAR UPDATE: Appetite Still Strong

Ample capital and need for yield to continue driving investment activity in 2022

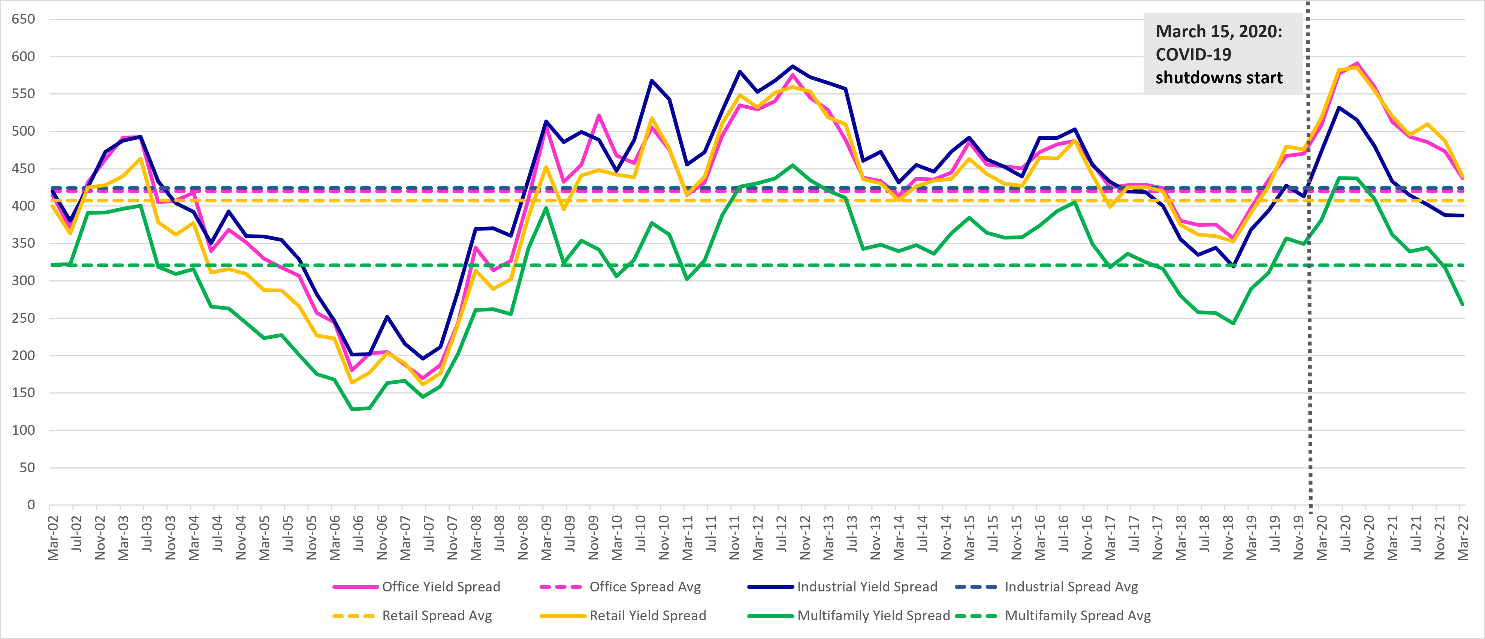

Following record-highs from 2021, commercial real estate activity has remained elevated in 2022 – led by multifamily, industrial and a strong rebound in retail. Despite widespread supply chain disruptions, inflation and political uncertainty around the war in Ukraine, investors were eager to unlock cash flow and pushed cap rates to record-lows in 4Q21 and 1Q22 across most sectors. Demand for real estate will continue to be strong for high-growth markets.

While interest in major metros (New York, Boston, Los Angeles) is returning for quality assets, focus on smaller markets continues to be front and center. While rising interest rates will eventually put upward pressure on cap rates, it has not slowed acquisition activity in smaller markets. Coldwell Banker Commercial professionals are still seeing tremendous amounts of capital pouring into secondary and tertiary markets in search of better yields and growth opportunities. The trifecta of corporate relocations, industrial expansion of large national brands, and greater retail openings in local neighborhoods is creating real growth potential that can support long-term demand for hard assets. So, despite today's record-high prices, most investors (save local developers) are more concerned about protecting existing wealth over thinning cap rate spreads. The need to put capital to work combined with a belief that rents can go higher to create positive leverage, and the natural hedge against inflation have been overriding rate hike fears.

Exhibit 1: Historical Cap Rate Yield Spread Over 10-Year U.S. Treasuries

Source: CBC Research, RCA

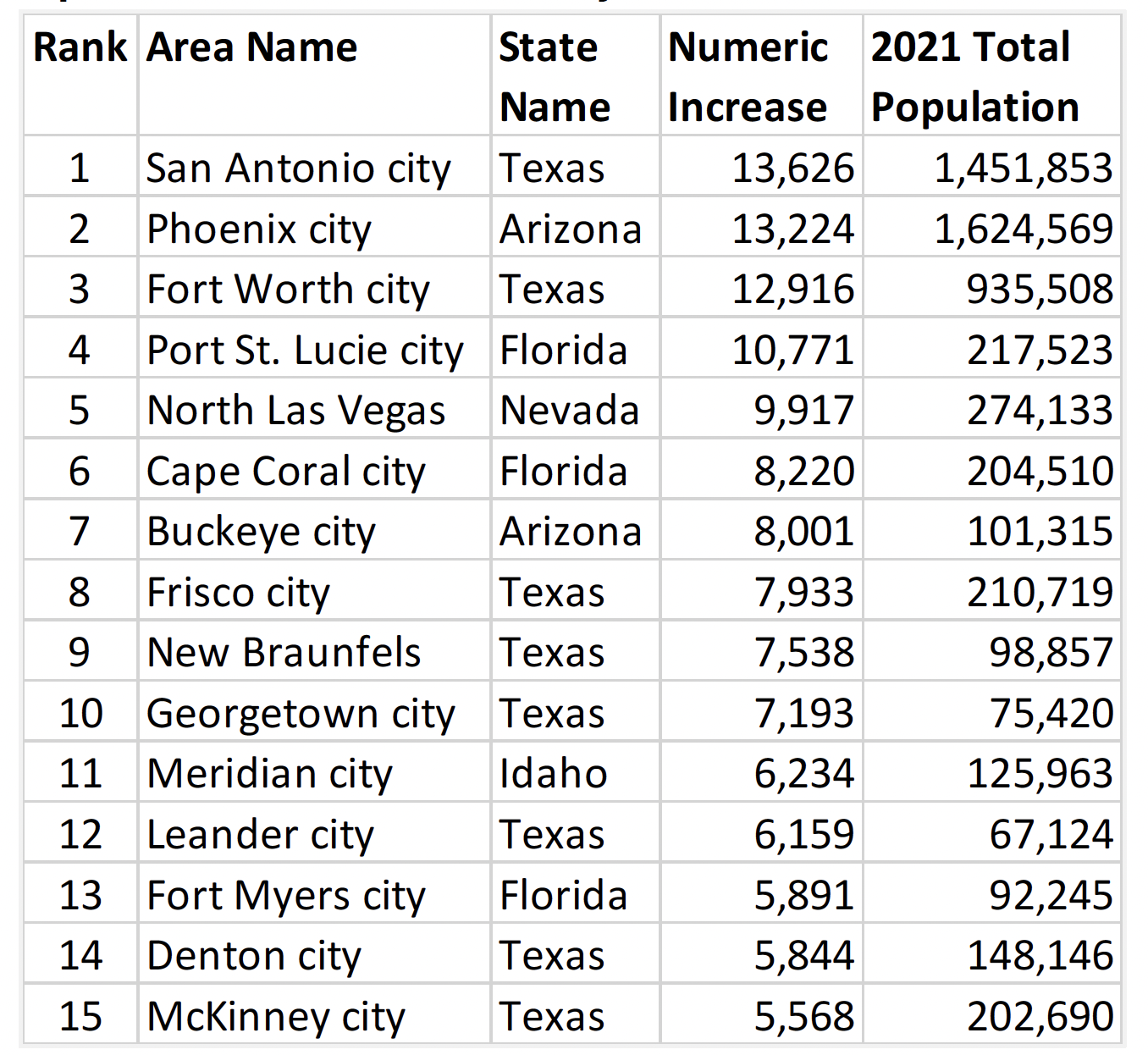

Lack of supply still driving demand. While buyers are becoming weary of high prices, appetite remains strong. However, sellers are not listing enough properties to satisfy the demand. Many still prefer to hold onto their assets (and cash in on rising rents) than grapple with the question of what to buy next. Only the institutions and retirees have been willing to sell; private and regional investors have not. Furthermore, construction pipelines have been hampered by severe labor shortages and still-rising material costs across the country. With more capital chasing too few deals, investors across the spectrum (high-net- worth individuals and family offices to REITS) are widening their searches into towns just outside of bigger cities (like Austin and Phoenix) as well as smaller metros (like Coeur d'Alene and Charleston).

Exhibit 2: The 15 Fastest-Growing Cities (between July 1, 2020 and July 1, 2021)

Population of 50,000+ on July 1, 2020

Source: CBC Research, US Census Bureau, municipal websites.

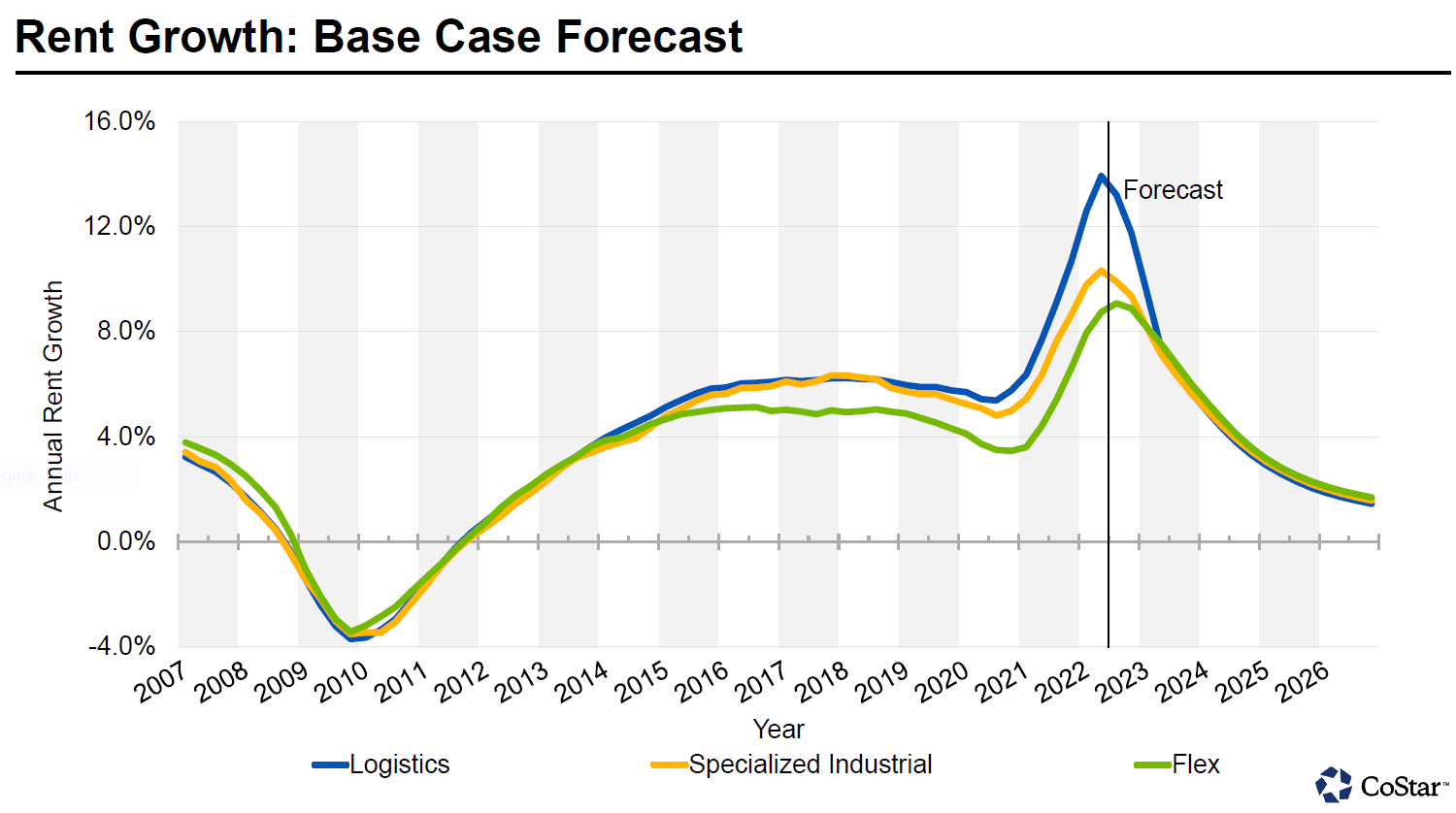

Market still hot for stable assets. Industrial, multifamily and medical offices continue to be the most active sectors. Extremely tight supply and near-zero vacancy rates have forced sales and rents to rise to record highs (according to CoStar). Smaller market economies are growing very fast as people who moved in from the big cities are now proving to be excellent consumers. Strong demand for online purchases of grocery and medicine, an uptick in last-mile delivery needs, and the shift toward just- in-case inventory continues to drive the need for industrial space. With most new construction preleased to corporate giants (like Amazon and UPS), finding 2500-5000 square foot facilities or land to build on has become a key focus for small- and mid-size businesses.

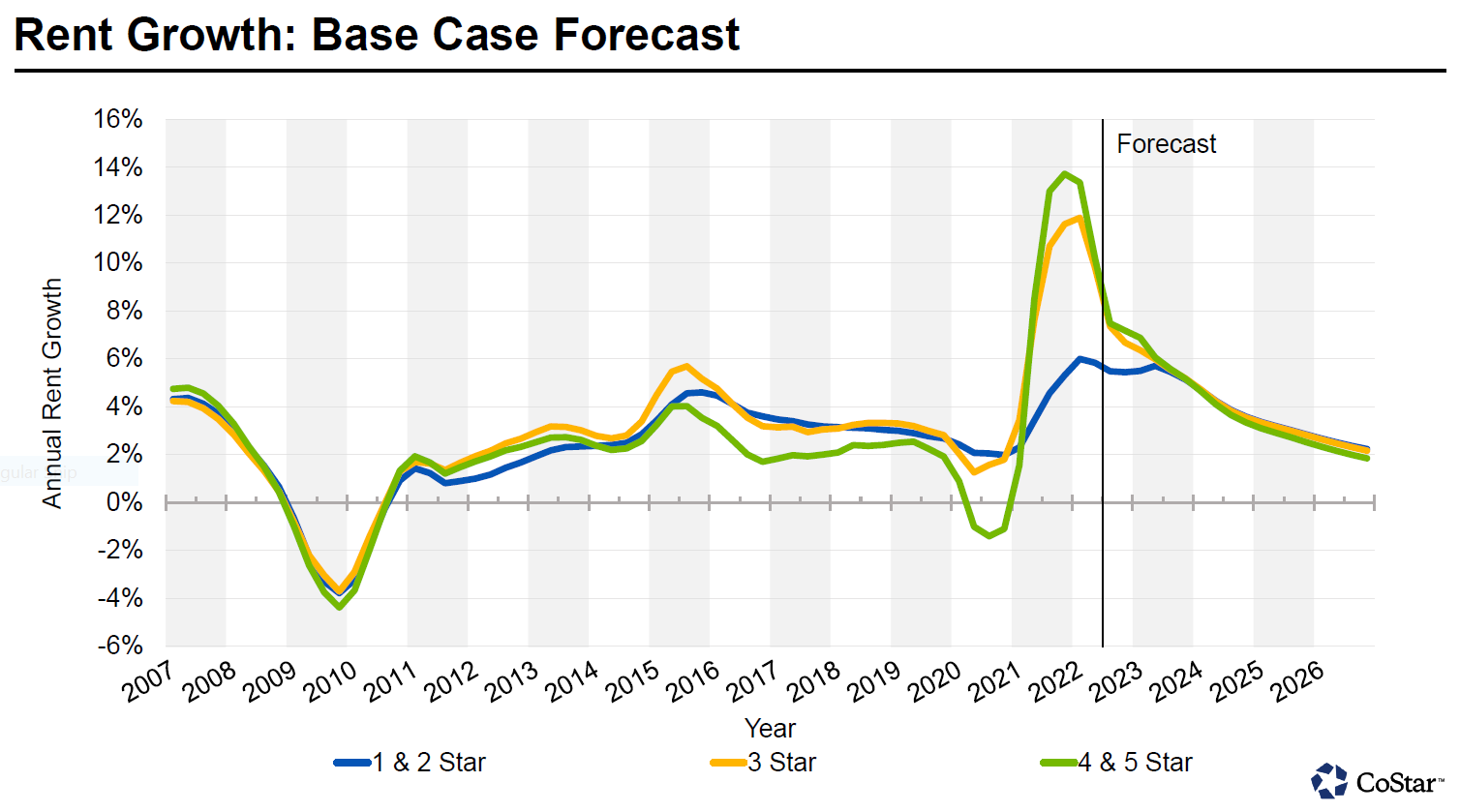

According to data posted on Trading Economics, multifamily is seeing a similar trend: rapidly rising mortgage rates (which doubled since January) are hitting existing home sales fast (-21.1% from January) and pushing demand for apartments and residential development land to unprecedented levels. With occupancy expected to remain above 95%, rent growth will likely outpace construction cost increases over the next year. Medical office buildings continue to be in high demand, following record-high rents and sales volume in 2021. Our commercial professionals are seeing strong owner-user demand for all types of medical and personal care spaces - from aestheticians to dentists, chiropractors and other specialists. Pent-up demand for doctors’ visits and elective procedures combined with growth in life science research will continue to drive new construction activity and acquisitions in 2022.

Exhibit 3: Industrial Rent Growth & Forecast

Source: CoStar (data through July 2022)

Exhibit 4: Multifamily Rent Growth & Forecast

Retail revival. The retail sector continues to undergo an evolution, with traditional big box spaces turning into fitness centers, restaurants, and experiential entertainment across the country. Appetite for both sales and leasing has taken off as COVID has become an accepted part of everyday life, with good triple-net locations getting quoted double their pre-pandemic pricing. We are seeing shortages of restaurant and retail shop space in many of our markets as franchisees look to open up their own independent businesses. While Class C and functionally obsolete centers may not fully recover, Class A and B centers are seeing demand soar - with a constant line of people inquiring if any openings will eventually come up.

The impact of WFH. While the office sector has started to improve, there is still a lot of uncertainty on when (or if) it will fully recover as many companies implement a hybrid work model and look for ways to cut back on square footage. To entice workers back to the office, companies will have to redesign the space for comfort and collaboration with built-in lounges, eateries, gyms, and open meeting space. Downtown locations will take a lot longer than the suburbs to recover as they sift through overbuilt stock and older buildings that are now being rehabilitated. Some of the hardest-hit cities (NYC, Chicago, San Francisco) are converting office buildings into condos, apartments and multistory warehouses. Suburban office markets, on the other hand, are faring better with lower available inventory and strong owner-user demand. Large urban office space will reflect high vacancy rates as long-term leases expire over the next 2-3 years. Downtown vacancies will begin to decline when there is full employee-employer acceptance of work-from-home and work-from-office approaches.

Construction costs starting to impact office leases. The cost to construct new space and the time it takes to bring in materials have jumped significantly over the past few months, driving rents up double and triple their pre-pandemic values. While this has not impacted leasing demand for retail and restaurant space, it has started to cause turmoil for office leases around major metro markets. Some decisions are being put on hold as companies consider alternative plans, while others need to renew their leases because they cannot move right now. Our commercial professionals are seeing the majority of tenants stay and renew – but for much shorter terms (1-2 years) – while they look for permanent space elsewhere.

Developers also hitting pause. While landlords have been able to raise rents significantly in 2022, we are starting to see enthusiasm wane among local developers as borrowing costs and high material prices are reaching a breaking point. Despite the low supply of available housing, economic uncertainty combined with severe labor constraints and building supply challenges are beginning to slow residential construction activity. With new construction yield spreads getting thinner, developers are turning to passive investments in smaller markets and taking longer to close deals. Small markets have been offering safer returns as new residents propel the local economies with the additional wealth amassed from the move. Our commercial professionals believe there is ability to continue raising rents, given households must live somewhere. The question is, which markets can keep the momentum going?

Conclusion. With a tremendous amount of capital pouring into emerging secondary and tertiary markets (which now house half the U.S. population – NAIOP), expect to see continued growth in industrial, multifamily, retail and suburban office assets. Developers and office users are starting to worry about yield spreads getting too thin, the momentum created by job gains, suburbanization and entertainment needs will create real consumer demand and growth that could offset some of the rising capital costs. Now that we are out of the easy money era, we will need to rely on higher rent growth to drive investment return. As with any business decision, the outlook for a specific property or property type depends on a variety of national and local conditions. Contact a commercial real estate professional to evaluate a particular situation.

Jane Thorn Leeson is a Research & Resources Analyst with Coldwell Banker Commercial.

Coldwell Banker Commercial®, provides commercial real estate solutions serving the needs of owners and occupiers in the leasing, acquisition and disposition of all property types. With a collaborative network of independently owned and operated affiliates, the Coldwell Banker Commercial organization comprises almost 200 companies and more than 3,000 professionals throughout the U.S. and internationally.

Updated: August 3, 2022

A Trusted Guide in Commercial Real Estate

Coldwell Banker Commercial® provides Commercial Real Estate Services from Property Sales and Leases, to Property Management. Learn how our expansive network of Independently Owned and Operated Affiliates and Real Estate Professionals use their in-depth knowledge of the local market and industry trends to help businesses and investors navigate the complexities of the commercial real estate landscape.